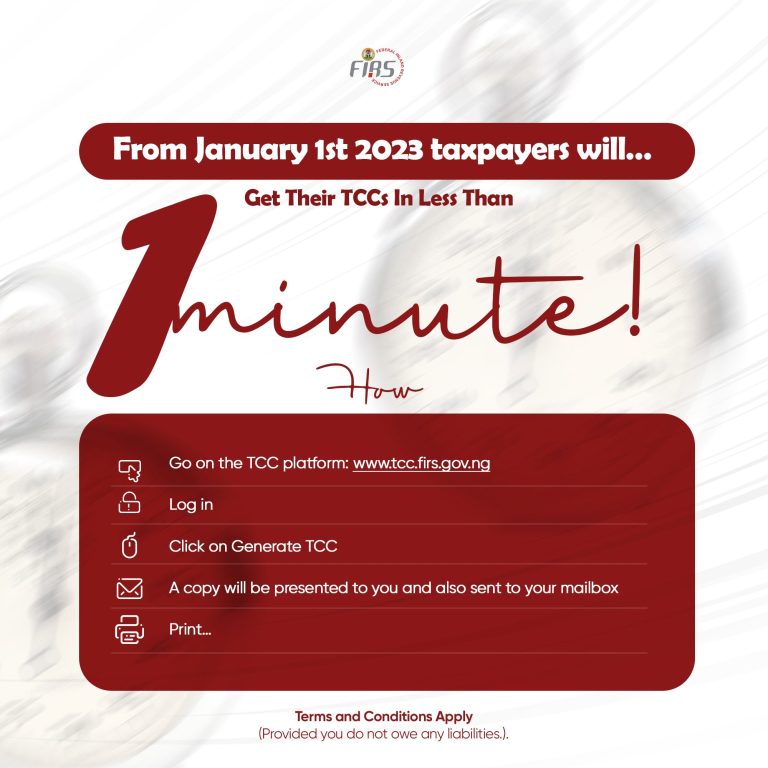

Tax is a compulsory charge by the government on goods, services, income, or profits of persons. There are different parameters for determining who, when, how, and where to pay taxes in Nigeria. After a taxable person registers with the revenue authority, the next step is to know the type and amount of tax to pay. Delaying the compliance cycle until the taxman issues a query may lead to more penalties. A good tax management system should optimize the tax structure and lower the exposure of a business. The article shows the types of taxes and levies in Nigeria payable to the following;

- Federal Inland Revenue Service (FIRS) only

- FIRS or the relevant State Internal Revenue Service

- Relevant State Internal Revenue Service

A – Taxes and levies administered by the Federal Inland Revenue Service only

1. Companies Income Tax

Incorporated entities are subject to Companies Income Tax on their profits from all sources. Exempt companies include an agricultural production company for a maximum period of eight years and a company with an annual turnover of ₦25million and below. The legislation for income tax exemption on approved industries or products is the Industrial Development (Income Tax Relief) Act [IDITRA]. Companies with a pioneer status will obtain a tax holiday from income tax for an initial period of three years. A company can get an additional holiday for one or two years. More details on FAQs on CIT is available here.

2. Hydrocarbon tax

Upstream petroleum companies will pay two types of income tax. They are companies income tax and hydrocarbon tax (HCT). HCT applies to crude oil, field condensates, natural gas liquids derived from associated gas, and produced in the field upstream of the measurement points. Hydrocarbon tax and ompanies income tax has replaced Petroleum Profit Tax. To read more on the Petroleum Industry Act 2021, click here.

3. Tertiary education tax

Resident companies in Nigeria pay tertiary education tax (TET) at 3% of the company’s assessable profit. Non-resident companies, small companies, and unincorporated businesses are exempt from TET. See the full article on TET

4. Value added tax

The rate of Value Added Tax (VAT) is 7.5% on the supply of VATable goods and services except for zero-rated or exempt items. To read more on Nigerian VAT, check here.

5.

National Information Technology Developmemt (NITDL) Levy

NITDL or Information technology levy is payable an annual turnover of one hundred million naira (₦100 million) and above. Companies covered are GSM service providers, telecommunications companies, cyber companies, internet service providers, pension managers, insurance companies, and financial institutions. The rate is one percent (1%) of profit before tax, and the levy is a deductible expense in a companies’ income tax computation.

6. Nigeria Police Trust Fund Levy

An annual levy of 0.005% of a company’s net profit is payable to the Nigeria Police Trust Fund. More details on the Police Trust Fund are here.

7. National Agency for Science and Engineering Infrastructure (NASENI) Levy

NASENI levy is payable by specific companies with an annual turnover of one hundred million naira (₦100,000,000). Companies operating in the banking, mobile telecommunications, information communications technology, aviation, maritime, and oil and gas sectors will pay NASENI levy. The rate is 0.25% of profit before tax.

B – Taxes payable either to the FIRS or the relevant State Internal Revenue Service

1. Withholding Tax

Withholding tax (WHT) is an advance payment of income tax. The rate is either 5% or 10%, depending on the nature of the transaction and the taxable person. The due date for filing WHT is 21 days following the month of the transaction.

2. Personal income tax

Personal Income Tax (PIT) covers taxation of employees, sole traders, individuals, partners, communities, families, trustees. Persons earning an annual minimum wage or below are exempt from personal income tax. Exempt income includes the income of government officials, diplomats, and local government institutions. Here is a Guide on PAYE taxes in Nigeria.

3. Capital Gains Tax (CGT)

CGT is payable on chargeable gains arising from the disposal of chargeable assets. The CGT law applies a rate of 10% applies to individuals and companies. CGT is remitted to the relevant tax authority.

4. Stamp Duty

Stamp duty is the tax payable on documents as a form of agreement or transaction between two or more persons. The rate is either fixed or variable, depending on the type of transaction.

C – Taxes and levies payable to the relevant State Internal Revenue Service only

1. Consumption Tax

The Hotel Occupancy and Restaurant Consumption Law govern consumption tax in Nigeria. The consumption tax rate is 5% on the value of goods and services consumed in hotels, restaurants, and event centres.

2. Levies

It includes annual development levy on employee as well as business premises levy.

D – Others

1. Custom and Excise Duties

Customs duties are payable on goods coming into Nigeria from 5% to 35% of import value. Excise duty is a charge on the production, sale, or use of certain locally produced goods.

2. Expatriate Employment Levy

A flat fee for companies who hire expatriate employees in Nigeria. The annual levy is payable to the Nigeria Immigration Service.

Conclusion

A medium sized business that generates income can pay three or more taxes in Nigeria to the revenue authority. Keeping track of the different tax laws in Nigeria can be tedious. Businesses must consider the tax impact of transactions to avoid extra costs. If you need help in managing your taxes in Nigeria, check BRC Tax Solutions.