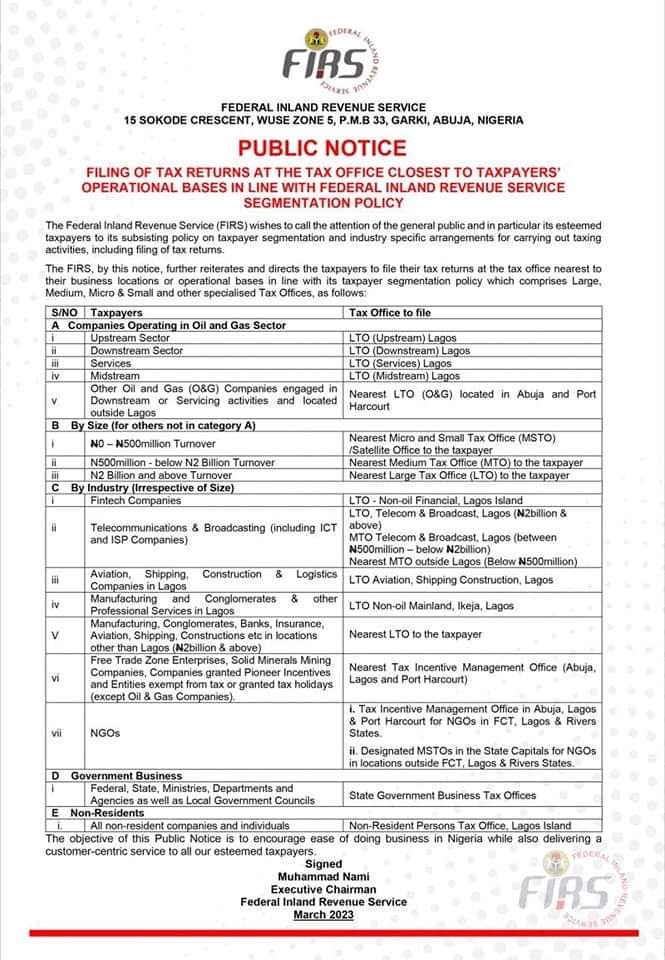

Federal Inland Revenue Service (FIRS) has issued a public notice that requires companies to deduct withholding tax (WHT) and value added tax (VAT) on payment to agents, dealers, distributors, and retailers. Companies, especially those in the Fast Moving Consumer Goods (FMCG) industry are expected to deduct WHT and VAT at the correct rates on compensation, commission, rebates, incentives or rewards. It includes payment in cash, credit note, goods-in-transit, and any other form. Thereafter, the company making payment will remit the tax payable to FIRS by the 21st day of each month. This Notice will change the tax impact of sales incentives to retailers and agents. How?

WHT is an advance payment of income tax. It is deductible at source on listed transactions and a taxable person can use the WHT credit to reduce the income tax liability. Commission, all types of contracts and agency arrangements, other than sales in the ordinary course of business are subject to WHT. The relevant provisions are the PITA, CITA, PPTA, and WHT Regulations. On the other hand, VAT is a tax on the supply of taxable goods and services. FIRS uses two methods to collect VAT. They are direct remittance and reverse-charge. The first scenario is when Business ABC issues a tax invoice to Customer XYZ.

Business ABC then remits the VAT directly to FIRS. However, there is an exception to direct remittance as shown in the second method. Under a reverse-charge, an authorized customer withholds and remits VAT on behalf of a supplier. Certain organizations must deduct VAT at source on payment to third parties. This applies to the three groups listed below.

- companies operating in the oil and gas sector

- government parastatals, ministries, agencies and departments

- businesses that use the services of a foreign company

Using the previous illustration, Business ABC supplied goods to the Ministry of Finance. The Ministry of Finance will withhold the VAT portion and remit same to FIRS on behalf of Business ABC. However, FIRS Information Circular No. 2006/02 provides further guidance on withholding tax rather than value added tax. The VAT Act is also silent on the deduction of VAT at source on commission paid to retailers. For instance, who bears the risk in case an agent or distributor fails to issue a VAT invoice?. Therefore, the public notice is inconsistent with the VAT provisions in the area of deducting VAT at source. FIRS’ notice further suggests that rebates are part of compensation so WHT and VAT should be deducted and remitted.

It appears that FIRS wants to ensure that VAT compliance moves beyond the issuance of a tax invoice to an actual collection of revenue. More so, the risk of non-compliance increases when a distributor belongs to the informal sector. To lower the impact, companies will act as authorized agents of the Federal Government for VAT collection. The new directive will also bring more taxpayers in the tax net, especially companies that grant rebates and discounts to distributors rather pay commissions. Before the notice, some companies may give discounts to retailers as it was not subject to WHT and VAT instead of paying taxes on commission.

In conclusion, stakeholders and companies will require more clarification on the directive. Please seek expert guidance on your business to prevent penalties. A copy of FIRS public notice on withholding tax and value added tax on payments to retailers is available here.

Editor’s pick….